People are busy and their time is precious. Companies looking to sell goods or services to people know this and work hard to make buying as convenient and easy as possible.

Any degree of friction that might cause a customer to defer or abandon their purchase must be avoided. Similarly, the opportunity to upsell relevant financial service products as part of the checkout process could be a new revenue generation opportunity.

Payments, access to capital, banking, and insurance are all examples of services that may be required when making a purchase. Traditionally, they also take time to organize.

Embedded finance solutions mean customers can access such related services simply and easily as part of the purchasing process.

Let's look closer at embedded finance, its different forms, and its benefits.

What is embedded finance?

Embedded finance means offering integrated financial services at online checkout or point of sale (POS). It generally involves non-financial institutions offering financial services to their customers.

Embedded finance products are usually provided via financial service providers. They are often regulated entities offering services with third-party branding or white-labeled basis.

The rise in eCommerce and online shopping has driven the fast evolution of embedded financing.

And now, thanks to new and easy-to-use technology such as APIs (application programming interfaces), embedded finance continues to grow.

Banking as a Service (BaaS)

Banking as a Service (BaaS) is a term that's often mentioned alongside - and confused with - embedded finance.

It refers to a business model that allows non-financial companies to offer financial services via partnerships with financial institutions. Without it, companies would have to directly obtain a banking license themselves.

So far, this sounds very similar - if not the same as - embedded finance, right?

The difference is nuanced but important.

Embedded finance vs BaaS

The key difference between embedded finance and BaaS is that embedded finance is focused on integrating financial services into existing products, while BaaS enables banks to offer their own financial services via third-party platforms.

Embedded finance is facilitated by BaaS, which also enables several other backend financial processes for banks and non-banks.

In other words, Baas is a prerequisite for embedded finance but it also covers unrelated areas.

Where in the buyer journey are embedded finance products introduced?

Embedded finance solutions are commonly implemented near the very end of the buyer's journey, i.e., just before they are due to make a payment.

This could occur across multiple platforms, including websites, physical in-store points of sale (POS), apps, and online marketplaces.

Overview of the embedded finance market

The embedded finance market is expanding rapidly. Some recent research estimates that its value will reach 183 billion USD by 2027 (which represents a growth of 183% from back in 2022).

Who provides embedded finance products?

Providers can range from traditional financial institutions to new fintechs. These may each offer services that target a range of different industries.

Companies such as Stripe, Plaid and Square emerged in the 2010s as leaders of the embedded finance market. They offered businesses simple APIs to integrate payments processing and other various financial tools into their customers' service offerings.

In recent years, the embedded finance market has expanded beyond fintech startups. Traditional financial institutions and technology companies are now involved in the embedded finance revolution. Examples include JPMorgan Chase, Goldman Sachs, and Amazon.

B2B vs B2C embedded finance

Many people associate embedded finance products with business-t0-consumer (B2C) solutions, such as BNPL for retail buyers.

However, companies in the business-to-business (B2B) also offer B2B-specific financing. And they also offer embedded finance products, including BNPL specifically for B2B buyers.

Types of embedded finance

If you are looking to launch an embedded finance project, there are many providers who can offer everything from traditional financial services to insurance.

The following list will help define embedded finance in terms of specific services that typically fall under this category.

1. Embedded payments

Embedded payments refers to the integration of payments processing live at the point of purchase, whether that's an eCommerce website, mobile application (app), or physical point-of-sale device. This is a very common and one of the earliest forms of embedded services but it continues to evolve.

When payments are directly embedded into an application or platform, users can make online banking transactions, without being redirected somewhere else.

Customer data is immediately processed and recorded by the merchant, which allows for seamless and streamlined transactions.

How embedded payments work

Embedded payments make financial transactions seem seamless, simple and instantaneous. The process involved is actually more complicated.

Here is a simplified outline of some of the main steps involved:

- Integration. Embedded finance needs to have been embedded within a platform to work using an API

- Tokenization. Sensitive information (credit card details, etc.) is encrypted and given a unique number or token when sent between parties involved in the payments process

- Verification. Initially, a financial service provider (the issuer processor) verifies the customer and their transaction

- Authorization. After verification, the merchant's bank confirms the transaction (via the acquirer processor)

- Settlement. The transferal of funds between the customer and the merchant's accounts (via their banks and processors) takes place over the following few days

Example of embedded payments

Businesses can add an Amazon Pay button to their online stores on third-party websites. It allows customers to use their Amazon account to make purchases on third-party websites.

Uber's payment acceptance is also embedded finance as the payment automatically takes place. Passengers can simply be on their way at the end of the journey.

These embedded payment solutions provide a seamless payment experience for customers and can increase conversion rates for businesses.

2. Embedded financing (/lending)

Embedded financing (or embedded lending) refers to the integration of loan products or financing options directly into a service or platform.

The lending service takes place through embedded bank accounts connected to stores or online platforms. The user can request a loan and receive a decision in real time without ever leaving the point-of-sale (POS).

It makes financing convenient by eliminating the need for customers to visit different websites or institutions to make loan applications. This can lead to businesses avoiding drop-outs, increasing sales and average order volumes (AOV).

It also enables lenders to access a larger customer base through their third-party relationships.

How embedded financing works

The embedded financing process works in approximately the following way:

- ntegration. The POS of the customer-facing business is integrated with a lending finance provider's (a financial institution) API. This enables the latter to access data related to a customer's transaction history and creditworthiness.

- Approval. When a customer seeks financing for a purchase, the lender's (financing provider's) technology analyzes the customer's data to determine their eligibility and the terms of the loan.

- Lending. If the loan is approved, the lender disburses the funds to the customer, allowing them to complete the initial transaction.

- Repayment. The customer repays the loan or credit back to the lender over a period of time, sometimes with interest and other fees.

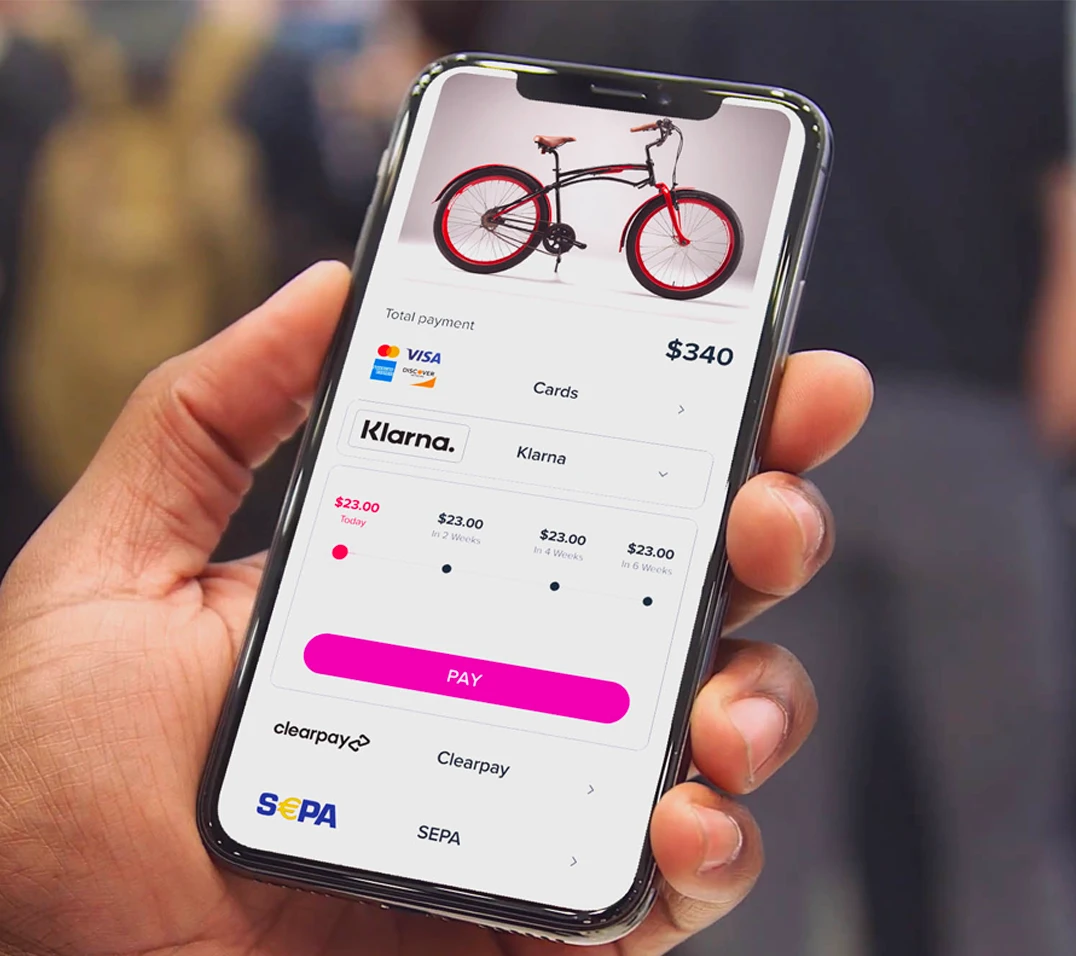

Buy now pay later (BNPL)

'Buy now, pay later' is perhaps the most well-known form of embedded financing.

BNPL programs allow customers to receive goods and then repay them in installments over time, rather than paying the entire amount upfront.

According to WorldPay, BNPL is on target to account for approximately 5.3 percent ($438 billion) of all global e-commerce transaction value by 2025.

Embedded financing in B2B

The B2B market has previously been regarded as having lower expectations of choice and convenience than B2C buyers. But as B2B buyers have seen payment options advance greatly in their experiences as a consumer, B2B expectations are now growing rapidly.

B2B transactions are generally less frequent but larger. They can often require the involvement of a number of departments and complex accounting process requirements.

3. Embedded banking

Embedded banking typically refers to when traditional banking services are provided to customers via non-financial services businesses.

The customer will often be unaware that these lending services are being provided by a third party, usually a traditional bank or fintech.

This can lead to the customer-facing business enjoying greater user engagement and retention. And it adds additional revenue streams through commission or transaction fees.

Compliance and credit risk are often controlled by the banking provider. This saves a lot of work for businesses, not least work involving attaining a banking license.

Examples of embedded banking services

There are several different kinds of embedded banking products. These include:

- Agency banking services

- Cross-border payments

- Virtual accounts

- Card issuing

Embedded banking is a B2B2C service

The embedded banking business model is essentially a hybrid of business-to-business (B2B) and business-to-consumer: B2B2C.

The bank providing the embedded banking services offers its solutions to a business or organization who then provides them to its own customers.

This set-up is particularly useful in the B2B market. Here, embedded banking accounts allow users to manage their payments, bills, and credit all within a single platform.

This capability can help businesses attract new customers and increase interaction and retention with existing ones.

4. Embedded insurance

Embedded insurance is insurance that can be purchased alongside a product or service at the physical POS or at checkout on their website, app, or online marketplace.

Its popularity in the commercial world has become evident over recent years. The travel industry is one such example: airlines, hotels, and other associated providers now routinely offer insurance at checkout.

A business can collaborate with an insurance provider to offer an insurance product. Or they can build their own in-house insurance department. Outsourcing is often a far quicker solution to deploy and avoids internal resources being diverted into non-core activities.

Making embedding insurance available can create greater user engagement and retention. It also provides additional revenue streams through commission or transaction fees.

And the benefits for the customer are clear: increased convenience, a more seamless user experience, potentially lower premiums, and better coverage alternatives.

Airport flight insurance (1960 - 2000s)

Flight insurance at airports is possibly the first example of embedded insurance. Vending machines were present in most airports in the 1950s and 1960s, especially in the US. They gradually declined and then disappeared over the following few decades.

They would supply instant insurance for individual passengers for the specific leg of their journey for a few dollars.

And it was a profitable business...

So profitable, that the New York State Insurance Department ordered vendors to decrease their premiums by 60%.

The technology behind embedded financial services

Embedded financial services rely on several types of technology to integrate their offers with businesses and financial infrastructure. Below is a brief outline of these.

1. Application programming interfaces (APIs)

A set of protocols and tools that enable different software applications to communicate with one another. Using APIs, developers can integrate services and functionalities across platforms

2. Cloud Computing

A model of computing that provides on-demand access to a shared pool of computing resources (such as servers) over the web. It allows users to scale resources up or down according to their needs

3. Artificial intelligence (AI) and machine learning (ML)

These technologies analyze financial data to provide customized insights and personalized financial advice to users

4. Blockchain

A distributed and decentralized digital ledger that records transactions in a secure, transparent, and immutable way.

It utilizes cryptography to provide secure and tamper-proof transactions for financial services such as remittances, digital currencies, and payment processing.

5. Data Analytics

Technologies are used to process large volumes of financial data, enabling financial service providers to offer personalized products and services to their customers

Embedded finance's role in eCommerce and digital spending

Global eCommerce market sales have grown dramatically in recent years. By some estimates, they look set to reach over 8.1 billion USD in 2026 - up from approximately 6.3 billion USD in 2023.

Because of this, financial services integration into e-commerce platforms is becoming increasingly vital. Businesses need to keep up with demand.

Many fintechs look set to disrupt established financial institutions by providing consumers with a range of innovative financial goods and services - including embedded finance-related ones.

The benefits of embedded finance

Embedded finance offers several advantages for businesses (proxy lenders), customers (borrowers), and traditional banks/fintechs (the ultimate lenders).

Some of the key benefits of embedded finance include:

1. Convenience

Embedded finance saves customers from needing to go to a bank or financial institution to get financial products and services.

This in turn can save businesses from having to offer longer payment terms or break down larger orders into small ones.

2. Revenue

Embedded finance can potentially increase profits for businesses. It can do this by attracting new customers and increasing the loyalty and average order volume (AOV) of existing ones. It can also help generate and diversify new revenue streams.

3. Cost savings

By eliminating the need to build compliance (such as gaining a banking license) or technology, embedded finance saves businesses money and time.

Customers can save costs by reducing shipping fees and gaining better rates or discounts on larger orders.

4. Personalization

Embedded finance can enable businesses to offer more personalized financial products and services to their customers.

They can use data to better understand and serve the specific needs and preferences of their customers.

5. Access

Embedded finance can make financial services accessible to individuals and organizations who did not previously have access to them.

And, more broadly speaking, it can increase credit access and inclusivity, especially in under-banked areas.

6. Security

By integrating payment processing into these platforms, businesses can also reduce the risk of payment errors and fraud.

This integration often includes several payment security features, including tokenization, authentication protocol, real-time fraud monitoring, and secure data exchanges.

Embedded finance platforms can use tokenization to protect sensitive payment information, such as credit and debit card last numbers, by replacing them with unique identifiers that are useless to hackers. This approach helps to prevent fraud and protect user data.

What does the future of embedded finance look like?

Further technological and consumer behavior trends are likely to influence the direction of embedded finance further.

A number of trends have emerged in recent years, including:

- Increased personalization

- Greater integration with non-financial services

- More decentralized and open systems

- Continued expansion in emerging markets

- Increased regulatory scrutiny

Some of these trends might first appear in the B2C field and then move into B2B. Others might appear in some geographies but not others.

Conclusion

Embedded finance integrates and streamlines financial processes into non-financial institutions, enabling them to offer financial services to their customers.

It usually operates near the end of the buyer's journey, just before they make a payment. The field has been enabled by advancements in technology and APIs, and companies such as Stripe, Plaid, and Square have emerged as market leaders for payments.

Traditional financial institutions and technology companies such as JPMorgan Chase, Goldman Sachs, and Amazon have also entered the market.

Embedded finance encompasses a wide range of organizations and industries, including business-to-consumer (B2C) and business-to-business (B2B) solutions. Services include:

- Embedded payments

- Embedded financing, including buy now pay later (BNPL)

- Embedded banking

- Embedded insurance

The embedded finance market is expected to continue expanding, with a projected value of USD 183 billion by 2027.